Key Findings

- Common-wage earners within the OECD have their take-home pay lowered by two main taxes: particular person earnings taxes and payroll taxes (each employee- and employer-side).

- Worth-added taxes (VAT) and gross sales taxes additionally place a taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of common authorities companies, items, and actions.

burden on take-home pay used for consumption. - Earlier than accounting for VAT and gross sales taxA gross sales tax is levied on retail gross sales of products and companies and, ideally, ought to apply to all ultimate consumption with few exemptions. Many governments exempt items like groceries; base broadening, reminiscent of together with groceries, may preserve charges decrease. A gross sales tax ought to exempt business-to-business transactions which, when taxed, trigger tax pyramiding.

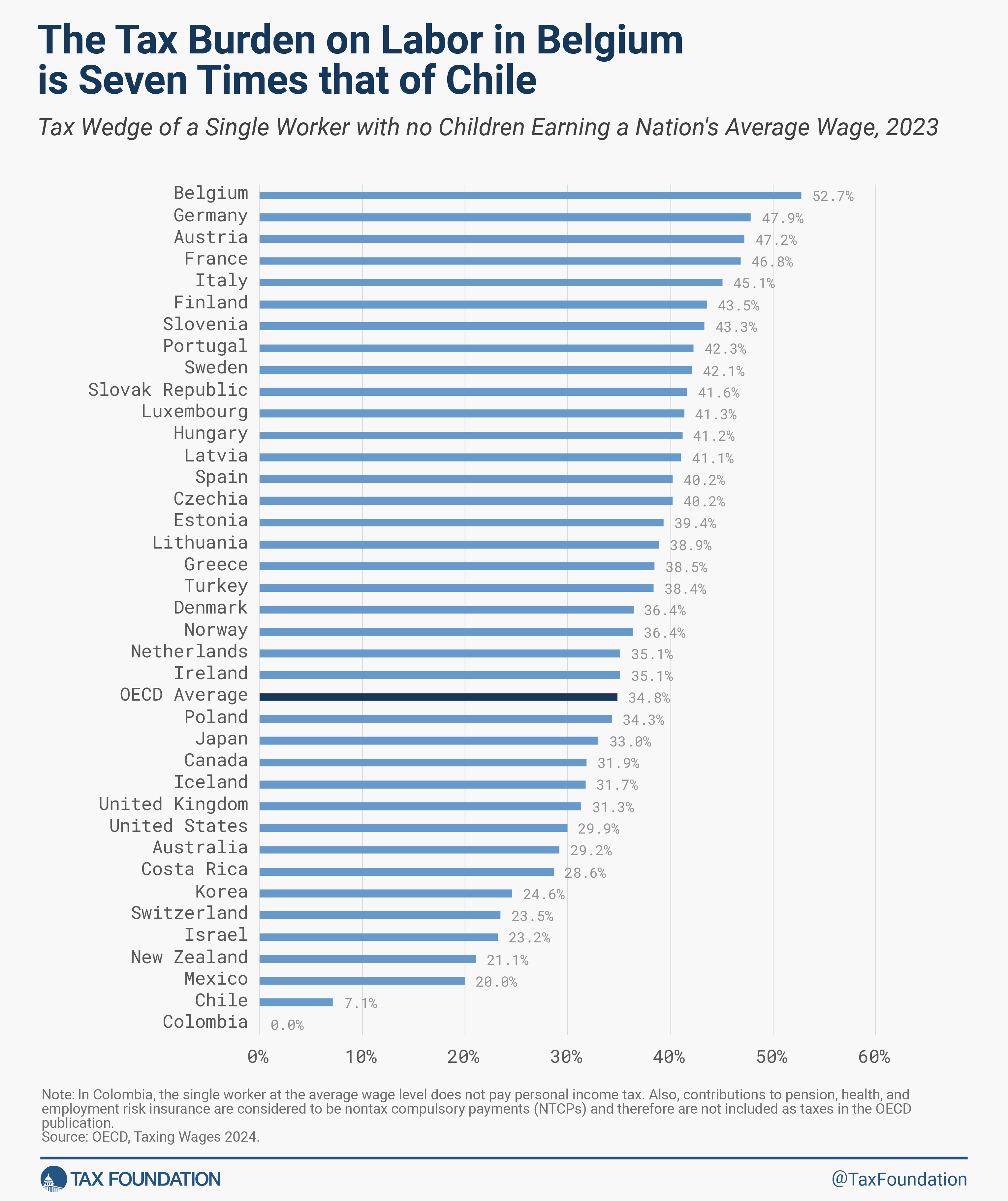

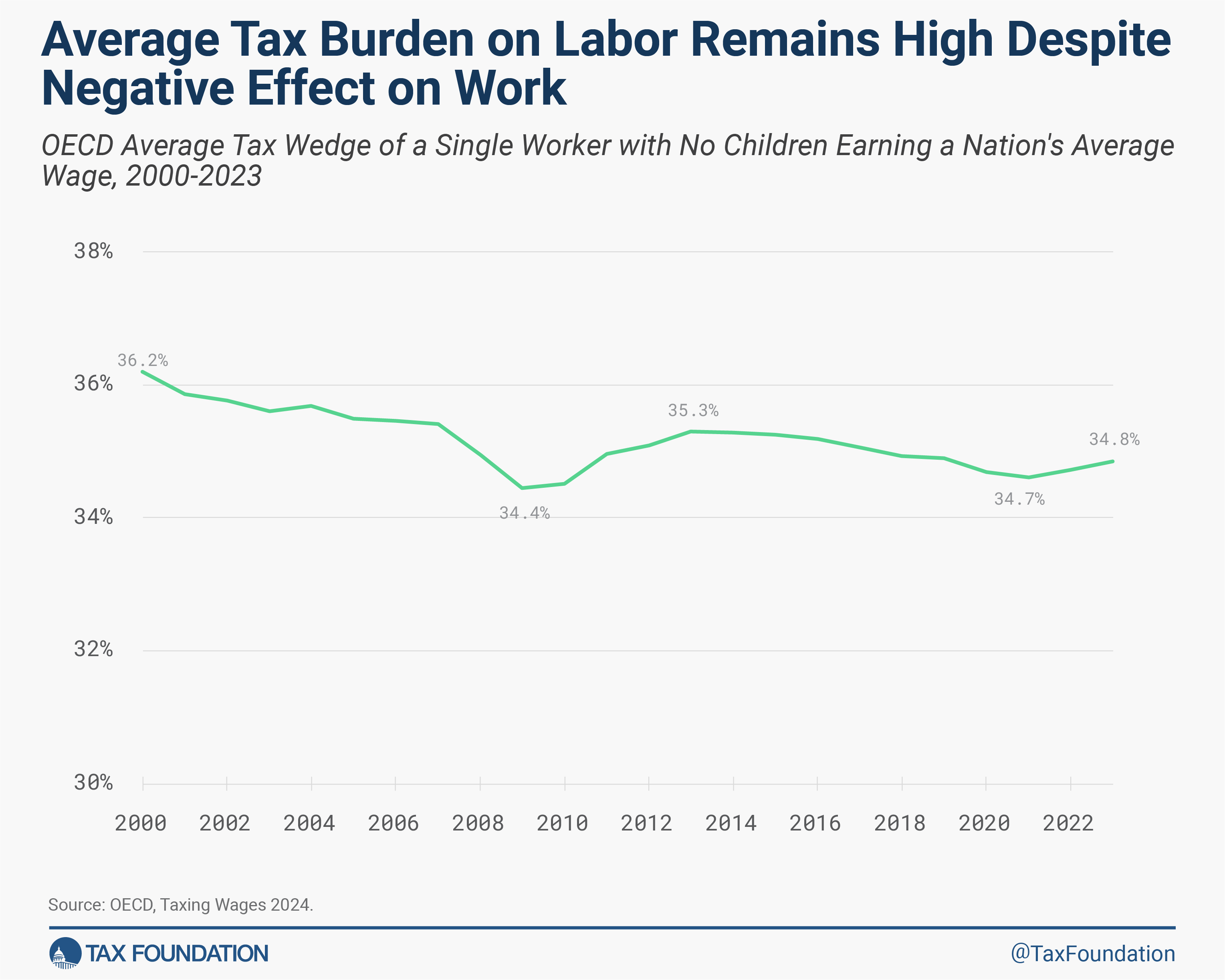

, the common tax burden a single, average-wage earner confronted within the OECD was 34.8 % of pre-tax earnings in 2023. The typical OECD tax burden on labor has dropped 1.4 share factors over the previous 20 years. - The typical tax burden amongst OECD nations varies considerably. In 2023, a employee in Belgium confronted a tax burden seven occasions greater than that of a Chilean employee.

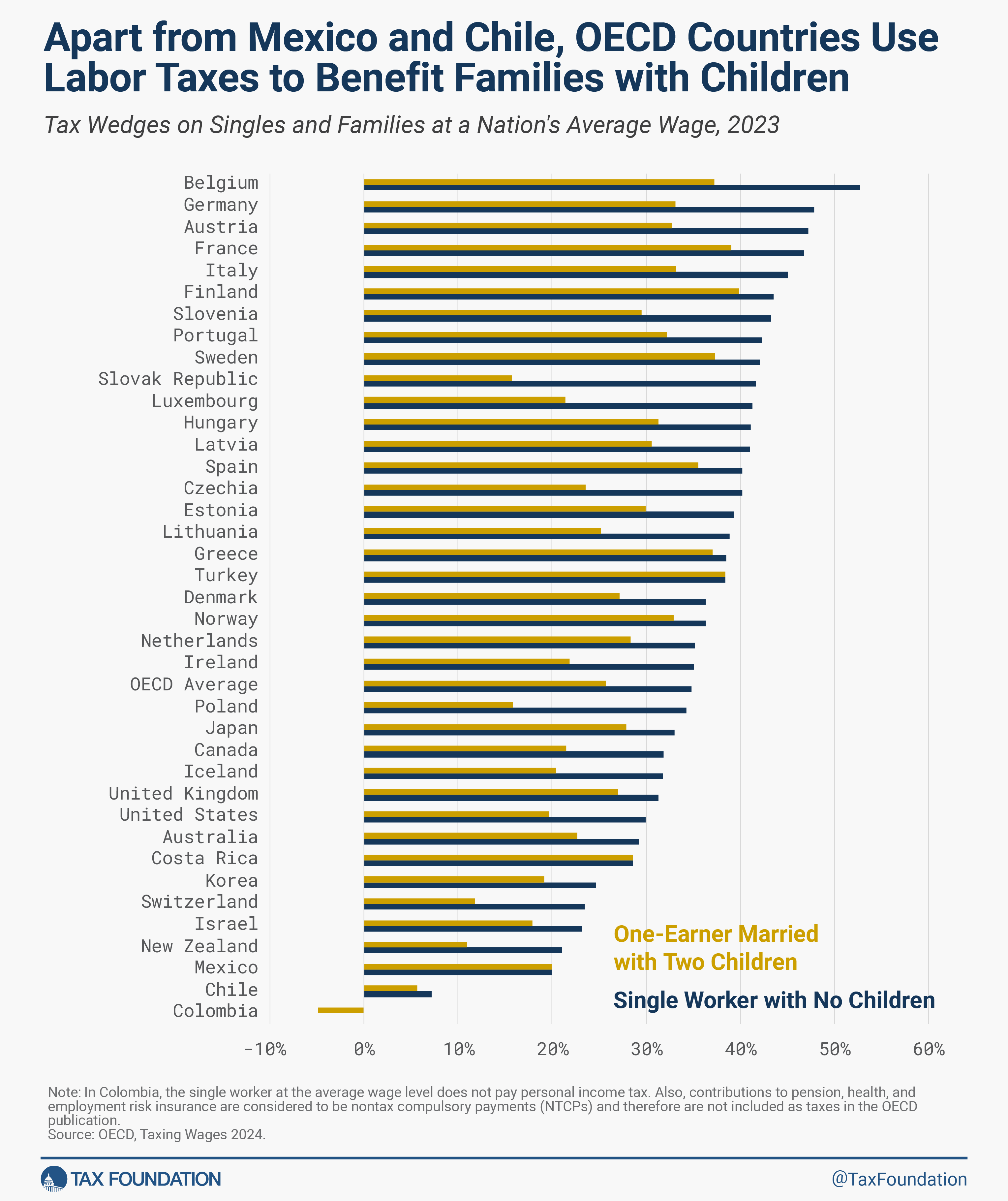

- In 2023, the common tax burden from earnings and payroll taxes for households in OECD nations was 25.7 %, 9.1 share factors decrease than for single taxpayers with out kids. Usually, nations with greater tax wedges present higher tax reduction for households with kids.

- Between 2021 and 2023, the OECD common tax burden elevated barely by 0.2 share factors. Due to this fact, all nations ought to index the earnings tax to inflationInflation is when the overall value of products and companies will increase throughout the financial system, lowering the buying energy of a foreign money and the worth of sure property. The identical paycheck covers much less items, companies, and payments. It’s generally known as a “hidden tax,” because it leaves taxpayers much less well-off as a result of greater prices and “bracket creep,” whereas growing the federal government’s spending energy.

to keep away from bracket creepBracket creep happens when inflation pushes taxpayers into greater earnings tax brackets or reduces the worth of credit, deductions, and exemptions. Bracket creep leads to a rise in earnings taxes with out a rise in actual earnings. Many tax provisions—each on the federal and state stage—are adjusted for inflation.

. - In 2023, an Italian employee making €34,832 ($54,843) confronted a marginal tax wedgeA tax wedge is the distinction between complete labor prices to the employer and the corresponding web take-home pay of the worker. It is usually an financial time period that refers back to the financial inefficiency ensuing from taxes.

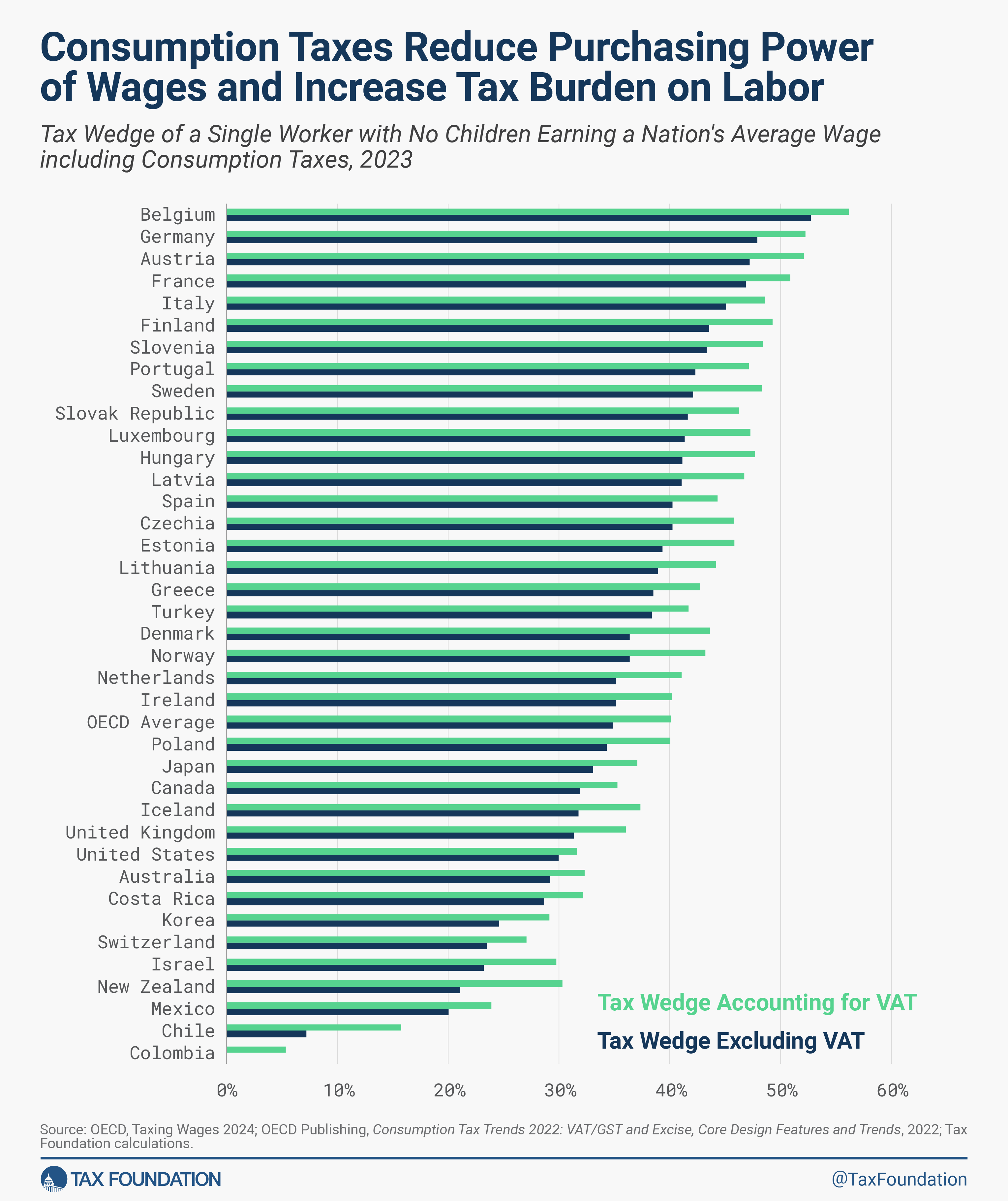

as excessive as 225 % on a 1 % improve in earnings. Such marginal tax wedges may deter employees from pursuing extra earnings and dealing additional hours. - Accounting for VAT and gross sales tax, the common tax burden on labor in 2023 was 40.1 %, 5.2 share factors greater than when solely earnings and payroll taxes are thought of.

Introduction

Particular person earnings taxes, payroll taxes, and consumption taxes make up a big portion of many nations’ tax income.[1] These taxes mixed make up the tax burden on labor each by taxing wages immediately and thru the tax burden on wages used for consumption.

The Organisation for Financial Co-operation and Improvement (OECD) reviews information on the composition of the tax burden on labor throughout 38 developed nations.[2] The newest information out there exhibits that, on common, single employees with no kids, incomes a nation’s common wage within the OECD, confronted a tax burden from earnings and payroll taxes of 34.8 % in 2023. After accounting for value-added taxes (VAT) and gross sales taxes, which scale back the buying energy of earnings, the OECD common tax wedge was 40.1 % in 2023.

In lots of nations, taxes are progressive, which signifies that higher-income employees are taxed at greater charges. Nonetheless, the common employee doesn’t essentially escape from being burdened by these taxes. It is usually necessary to notice that the tax burden on households is commonly decrease than the burden on single, childless employees incomes the identical pretax earnings.

As famous in our primer[3] on the tax wedge on labor, there’s a unfavorable relationship between the tax wedge and employment. Due to this, nations ought to discover methods to make their taxation of labor much less burdensome to enhance the effectivity of their labor markets.

The Tax Burden on Labor

The tax burden on labor is known as a “tax wedge,” which merely refers back to the distinction between an employer’s price of an worker and the worker’s web disposable earnings. For the aim of the OECD research, the wedge is set by a number of elements: the quantity of pre-tax earnings (known as “labor price”) of a employee, the taxes that apply to that earnings, and whether or not the taxpayer is submitting as single or as a household.

The OECD calculates the tax burden by including collectively the earnings tax fee, employee-side payroll taxA payroll tax is a tax paid on the wages and salaries of workers to finance social insurance coverage applications like Social Safety, Medicare, and unemployment insurance coverage. Payroll taxes are social insurance coverage taxes that comprise 24.8 % of mixed federal, state, and native authorities income, the second largest supply of that mixed tax income.

fee, and employer-side payroll tax fee of a employee incomes the common wage in a rustic. The OECD then divides this determine by the full labor price of this common employee, or what the employee may have earned within the absence of those three taxes.

Private Earnings Taxes

Private earnings taxes are levied immediately on a person’s earnings, together with wage earnings. These taxes are usually levied in a progressive method, which means that a person’s common tax chargeThe typical tax charge is the full tax paid divided by taxable earnings. Whereas marginal tax charges present the quantity of tax paid on the subsequent greenback earned, common tax charges present the general share of earnings paid in taxes.

will increase as earnings will increase. The quantity of earnings tax paid usually additionally depends upon whether or not the taxpayer is submitting as single or as a household, as most nations enable for some focused tax reduction for households with kids.

Payroll Taxes

Payroll taxes are usually flat-rate taxes levied on wages and are along with the taxes on earnings. In most OECD nations, each the employer and the worker pay payroll taxes. These taxes normally fund particular social applications, reminiscent of unemployment insurance coverage, medical health insurance, and previous age insurance coverage.

The Financial Incidence of Payroll Taxes

Though payroll taxes are usually cut up between employees and their employers, economists usually agree that either side of the payroll tax finally fall on employees.

In tax coverage, there is a vital distinction between the “authorized” and the “financial” incidence of a tax. The authorized incidence of a tax falls on the occasion that’s legally required to write down the test to the tax collector. Nonetheless, the occasion that legally pays a tax just isn’t all the time the one which finally bears the burden of the tax. The “financial” incidence of a tax can fall on any variety of folks and is set by the relative elasticities of provide and demand of a taxed good, or how folks and companies reply to a tax.[4]

Common OECD Tax Burden

In 2023, the common OECD tax wedge for a single employee with no kids incomes a nation’s common wage was 34.8 %. The typical annual complete labor price per employee was $65,214. Earnings taxes accounted for 13.3 % ($8,703) of the labor price. Worker-side payroll taxes made up 8.1 % ($5,295) and employer-side payroll taxes made up 13.4 % ($8,731). The typical annual disposable after-tax earningsAfter-tax earnings is the online quantity of earnings out there to take a position, save, or eat after federal, state, and withholding taxes have been utilized—your disposable earnings. Corporations and, to a lesser extent, people, make financial selections in mild of how they will finest maximize their earnings.

of a employee within the OECD amounted to $42,486, or 65.1 % of complete labor price.[5]

Tax Burden by OECD Nation

The OECD common described above displays the general tendencies of the tax burden on labor among the many 38 OECD nations. Nonetheless, as proven under, many nations deviate from this common fairly considerably, reflecting financial and coverage variations throughout nations.

Single Employee with No Youngsters

In 2023, the tax wedge confronted by single employees with out kids ranged from solely 7.1 %[6] in Chile to 52.7 % in Belgium, a distinction of 45.6 share factors. Fifteen nations had a tax wedge above 40 %, 13 nations between 40 and 30 %, and 10 nations under 30 %.

Tax wedges are significantly excessive in European nations—the 24 nations with the best tax burden within the OECD are all European. In distinction, 10 out of the 14 OECD nations with the bottom tax burden are non-European (the 4 European nations on this class are the UK, Switzerland, Iceland, and Eire).

In 30 out of 38 OECD nations, complete payroll taxes accounted for a bigger share of the tax burden on labor than earnings taxes did.[7] Australia, Canada, Denmark, Iceland, Eire, New Zealand, and the USA have been the one nations through which the share from earnings taxes exceeded payroll taxes. And worker payroll taxes accounted for a bigger share of the tax burden on labor than employer payroll taxes in seven OECD nations—Chile, Germany, Hungary, Israel, Lithuania, Poland, and Slovenia. Lithuania is the one nation within the OECD that reformed payroll taxes by together with the employer payroll tax within the complete labor price. Since 2019, employer payroll taxes have been paid by the worker, making all workers conscious of the particular tax burden on labor.

Evaluating a Single Employee with No Youngsters to a Married Employee with Two Youngsters

Most nations within the OECD present some focused tax reduction for households with kids, usually by way of decrease earnings taxes. The typical wedge for households, outlined as a one-earner married couple with two kids, was 25.7 % in 2023, in comparison with a median tax wedge of 34.8 % for single employees with out kids.

The next determine compares the tax burden confronted by a one-earner married couple with two kids with that of a single employee with out kids.

Usually, nations with a better tax wedge present higher tax reduction for households with kids. Germany, Austria, Slovenia, and Slovakia, which had the second, third, seventh, and tenth highest tax wedges for single employees with out kids, drop greater than seven positions, rating ninth, eleventh, sixteenth, and thirty-fifth, respectively, as soon as household reduction is included.

In 2023, the best household tax wedge was in Finland at 39.8 %, adopted by France at 39.1 %, whereas the bottom household tax wedge was in Chile at 5.7 %.

Slovakia has the biggest disparity between its 41.6 % wedge for single employees and 15.7 % wedge for households—a distinction of 25.9 share factors. Costa Rica, Mexico, and Turkey are the one nations that don’t present any tax reduction for households with kids. Nonetheless, Costa Rica and Mexico preserve the common tax wedge low.

OECD Tax Burden from 2000 to 2023

Though the tax wedge has modified fairly considerably in some nations over time, the common OECD tax burden on labor has dropped simply 1.4 share factors over the previous 20 years. In 2000, the common OECD tax wedge was 36.2 %, in comparison with 34.8 % in 2023. Nonetheless, the bottom stage was reached within the 2009 after the monetary disaster. Between 2021 and 2023, the common OECD tax burden elevated barely by 0.2 share factors. This slight improve exhibits the significance of indexing the earnings tax to inflation to keep away from bracket creep.

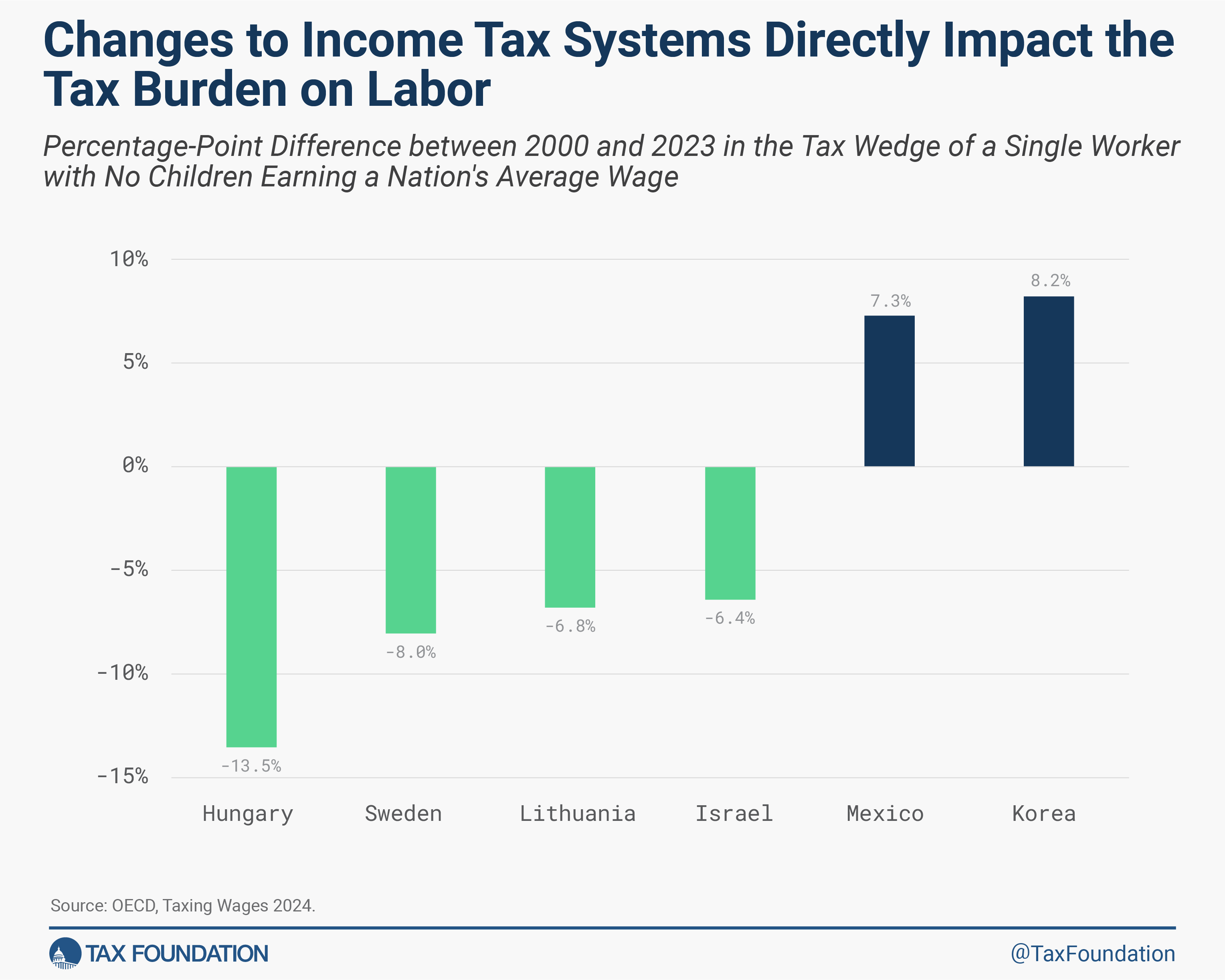

Most Notable Modifications within the Tax Burden since 2000

Some particular person nations have made substantial modifications to their earnings and payroll taxes within the final 20 years. The next graph exhibits the OECD nations with the biggest will increase and reduces of their respective tax wedges.

Hungary, the OECD nation with the best tax burden on labor in 2000, has had probably the most notable lower in its tax wedge, from 54.7 % to 41.2 % in 2023. That is partially because of the introduction of a flat taxAn earnings tax is known as a “flat tax” when all taxable earnings is topic to the identical tax charge, no matter earnings stage or property.

on earnings, which lowered the earnings tax burden relative to complete labor prices. Moreover, Hungary decreased its payroll taxes relative to complete labor prices. Israel, Lithuania, and Sweden have additionally lowered their tax burden on labor considerably, with a discount between 6.4 and eight share factors every.

South Korea has seen the best improve in its tax wedge since 2000, with a further tax burden of 8.2 share factors. Payroll and earnings taxes have elevated by 4.9 and 4.6 share factors since 2000. The tax wedge has additionally elevated in Mexico, by 7.3 share factors. Whereas payroll taxes relative to complete labor prices have roughly stayed the identical in Mexico, earnings taxes as a % of complete labor prices have elevated from 1 % in 2000 to 9.6 % in 2023.

Marginal and Common Tax Wedges

Evaluating the tax wedge on the common employee throughout nations is just a partial illustration of how taxes on labor affect the financial system, each by altering incentives to work and by elevating income for the federal government at numerous ranges.

The OECD’s Taxing Wages 2024 report presents each common and marginal tax wedges (MTW). The typical tax wedge is what has been introduced to date and is the mixed share of labor and payroll taxes relative to gross labor earnings, or the tax burden. The marginal tax wedge, however, is the share of labor and payroll taxes relevant to the subsequent greenback earned and may affect people’ selections to work extra hours or take a second job. The marginal tax wedge is mostly greater than the common tax wedge because of the progressivity of taxes on labor throughout nations—as employees earn extra, they face a better tax wedge on their marginal greenback of earnings. Nonetheless, a drastic improve within the marginal tax wedge, particularly at decrease ranges of earnings, may deter employees from pursuing extra earnings and dealing additional hours.

To test for doable spikes, the marginal tax wedge has been analyzed for gross earnings that vary between 50 and 150 share factors of the common wage in every OECD nation.[8]

An Austrian employee faces a marginal tax wedge of 85 % for a 1 % improve in gross earnings on prime of the gross annual wage of $41,108 (€30,824). It’s because the worker’s unemployment insurance coverage strikes to a distinct charge at this stage of earnings (month-to-month earnings of $2,971 or €2,228).[9]

A French employee will face a marginal tax wedge of 93 % for a 1 % improve in gross earnings on prime of the gross annual wage of $72,497 (€51,691). It’s because employer social safety contributions improve by 6 share factors at this stage of earnings.[10]

Of the three nations, an Italian employee will see the most important tax charge spike and face a marginal tax wedge of 225 % for a 1 % improve in gross earnings on prime of the gross annual wage of $54,843 (€34,832). It’s because the worker social safety contributions have been temporally decreased for the yr 2023 by 4 share factors as much as an annual earnings of $55,108 (€35,000).[11]

This exhibits that progressive taxA progressive tax is one the place the common tax burden will increase with earnings. Excessive-income households pay a disproportionate share of the tax burden, whereas low- and middle-income taxpayers shoulder a comparatively small tax burden.

charges and several other layers of social safety contributions can create marginal tax chargeThe marginal tax charge is the quantity of extra tax paid for each extra greenback earned as earnings. The typical tax charge is the full tax paid divided by complete earnings earned. A ten % marginal tax charge signifies that 10 cents of each subsequent greenback earned could be taken as tax.

spikes that may distort or change incentives to work.

Tax Burden Together with VAT

The tax burden on labor is broader than private earnings taxes and payroll taxes. In lots of nations, people additionally pay a value-added tax on their consumption. As a result of a VAT diminishes the buying energy of particular person earnings, a extra full image of the tax burden ought to embody the VAT. Though the USA doesn’t have a VAT, state gross sales taxes additionally diminish the buying energy of earnings.

Accounting for VAT charges and bases in OECD nations will increase the tax burden on labor by 5.2 share factors on common in 2023. The efficient VAT charge is far decrease than the statutory charge for every nation due to exclusions within the tax baseThe tax base is the full quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slender tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges.

. The distribution of VAT-inclusive tax wedges throughout nations is just like that proven in Determine 2.

In 2023, the nation with the biggest distinction between the 2 measures was New Zealand, with a tax wedge accounting for the VAT of 30.3 %, 9.3 share factors bigger than the tax wedge accounting just for earnings and payroll taxes.

The US had the smallest distinction between the 2 measures at 1.7 share factors. That is partially as a result of its gross sales tax charges are usually a lot decrease than VAT charges in different OECD nations.

Tax Burden in Europe

Though the tax wedge in Europe is mostly excessive, there’s a comparatively wide selection. The next map illustrates how European nations differ of their tax burden on labor.

In 2023, the common tax wedge of the 27 European nations coated in Determine 7 was 39.8 % for a single employee with out kids, in comparison with the OECD common of 34.8 %. Belgium had the best tax burden on labor at 52.7 % (additionally the best of all OECD nations), whereas Switzerland had the bottom tax burden at 23.5 %.

Conclusion

In 2023, single, average-wage employees paid about one-third of their wages in taxes. Between 2021 and 2023, the OECD common tax burden elevated barely, stressing the significance of indexing the earnings tax to inflation to keep away from bracket creep. In most OECD nations, households had smaller tax burdens than single employees with out kids incomes the identical earnings, however how a lot much less diversified. To advertise transparency and make the tax wedge seen to employees, nations ought to comply with Lithuania’s instance and embody the employer payroll tax within the complete labor price. Accounting for consumption taxes reveals greater tax wedges than simply accounting for earnings and payroll taxes. Governments with greater taxes usually justify their excessive tax burdens with extra in depth public companies. Nonetheless, the price of these companies will be greater than half of a median employee’s wage, and for a lot of, at the very least a 3rd of their wage.

Appendix

Methodology

Tax Wedges Accounting for VAT

The components for calculating tax wedges accounting for VAT makes use of the VAT charges and the VAT income ratio (VRR) from the OECD’s Consumption TaxA consumption tax is often levied on the acquisition of products or companies and is paid immediately or not directly by the patron within the type of retail gross sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an earnings tax the place all financial savings is tax-deductible.

Developments 2022: VAT/GST and Excise, Core Design Options and Developments.[12] We first calculate the tax-inclusive VAT charge, which is VAT charge/(1 + VAT charge). Subsequent, we multiply the tax-inclusive VAT charge by the VAT income ratio and by the full labor price to calculate the VAT quantity. The components for calculating the tax wedge together with the VAT is then:

VAT/gross sales taxes are in each the numerator and the denominator as a result of the tax wedge is taxes on labor as a share of complete labor prices. For workers, VAT/gross sales taxes are a part of taxes on labor, and they’re additionally a part of the full labor prices that employers face. By definition, a VAT is the speed of tax positioned on the worth added by a enterprise by using capital and labor. The added worth is measured by the distinction between the acquisition value of supplies and the sale of these supplies (most frequently after a enterprise turns these supplies into one thing extra helpful). Although companies could elevate costs to cross the price of a VAT or gross sales tax on to customers within the brief run, over the long term, the financial incidence of the VAT falls on employees.[13]

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

Subscribe

[1] Cecilia Perez Weigel and Daniel Bunn, “Sources of Authorities Income within the OECD, 2024 Replace” Tax Basis, Mar. 18, 2024, https://taxfoundation.org/information/all/world/oecd-tax-revenue-by-country-2024/.

[2] OECD Publishing, Taxing Wages 2024, https://www.oecd.org/tax/taxing-wages-20725124.htm.

[3] Scott A. Hodge and Bryan Hickman, “The Significance of the Tax Wedge on Labor in Evaluating Tax Techniques,” Tax Basis, 2018, https://information.taxfoundation.org/20190516115623/The-Significance-of-the-Tax-Wedge-on-Labor-in-Evaluating-Tax-Techniques.pdf.

[4] Congressional Funds Workplace, “The Distribution of Family Earnings, 2019,” Nov. 15, 2022, https://www.cbo.gov/publication/58353.

[5] Particular person gadgets could not sum to complete due to rounding. All U.S. greenback quantities on this report are U.S. {dollars} in buying energy parity (PPP).

[6] In Colombia, the one employee on the common wage stage doesn’t pay private earnings tax. Additionally, contributions to pension, well being, and employment danger insurance coverage are thought of to be nontax compulsory payments (NTCPs) and subsequently are usually not included as taxes within the OECD publication.

[7] See Desk 2 within the Appendix.

[8] On this case the OECD calculated the marginal charges by growing gross earnings by 1 share level as a way to scale back the variety of calculations as marginal charges wanted to be calculated for each single foreign money unit throughout the earnings vary included.

[9] OECD Publishing, Taxing Wages 2024, https://www.oecd-ilibrary.org/sites/dbcbac85-en/1/3/2/2/index.html?itemId=/content/publication/dbcbac85-en&_csp_=e795e241109a37e856f37ec39c7edba2&itemIGO=oecd&itemContentType=book#component-table-d1e142714-75d81c6094.

[10] Employer contribution tax charge for sickness, being pregnant, incapacity, and dying is 7 %, as much as 2.5 occasions the minimal wage. For wages that exceed 2.5 occasions the minimal wage, a 13 % charge applies. See OECD Publishing, Taxing Wages 2024.

[11] OECD Publishing, Taxing Wages 2024, https://www.oecd-ilibrary.org/sites/dbcbac85-en/1/3/2/19/index.html?itemId=/content/publication/dbcbac85-en&_csp_=e795e241109a37e856f37ec39c7edba2&itemIGO=oecd&itemContentType=book#section-d1e180850-cef3752885.

[12] OECD Publishing, Consumption Tax Developments 2022: VAT/GST and Excise, Core Design Options and Developments, 2022, https://doi.org/10.1787/6525a942-en. The newest OECD information out there for the VAT income ratio is from 2020. VAT charges are from 2023. The U.S. gross sales tax charge is the common of all U.S. state gross sales tax charges (weighted by inhabitants); see Jared Walczak, “State and Native Gross sales Tax Charges, Midyear 2023,” Tax Basis, Jul. 17, 2023, https://taxfoundation.org/information/all/state/2023-sales-tax-rates-midyear/. The U.S. gross sales tax income ratio was calculated because the ratio of the implicit gross sales tax base to state private earnings.

[13] Eric Toder, James R. Nunns, and Joseph Rosenberg, “Implications of Totally different Bases for a VAT,” Tax Coverage Heart and The Pew Charitable Trusts, Feb. 14, 2012, https://www.taxpolicycenter.org/publications/implications-different-bases-vat/full.

Share