Up to date for tax yr 2025.

Because the child boomer era ages, extra taxpayers are dealing with property and belief taxes for the primary time. In accordance with Accounting Today, the variety of earnings tax returns for estates and trusts (Kind 1041) elevated by 14.9% between 2020 and 2021. However for many people, dealing with taxes for an property or belief can really feel like deciphering a international language.

As extra individuals navigate these tax kinds, it’s necessary to grasp IRS Kind 1041 and its intricacies. This information will stroll you thru the necessities, breaking down Kind 1041 submitting necessities, directions, and tricks to make your tax preparation much less daunting.

At a look:

- Revenue generated between the proprietor’s loss of life and asset switch to beneficiaries have to be reported to the Inside Income Service on Kind 1041.

- Beneficiaries are answerable for paying earnings tax if belongings are distributed earlier than incomes earnings.

- Not all trusts and estates should file Kind 1041 — solely these with income-producing belongings or nonresident alien beneficiaries.

- The due date for Kind 1041 relies on the tax yr, which might be the calendar yr or a fiscal yr chosen by the executor.

What’s IRS Kind 1041?

IRS Kind 1041 is the U.S. Revenue Tax Return for Estates and Trusts. It’s used to report earnings earned by a decedent’s property or belief after the property proprietor’s date of loss of life however earlier than belongings are distributed to beneficiaries. Simply don’t confuse Kind 1041 with Form 706, which is used for submitting an property tax return.

When an individual passes away, their property turns into a separate taxable entity. Any earnings this entity earns — from rental earnings, capital features, curiosity, or dividends — have to be reported on IRS Kind 1041. Equally, earnings earned by sure trusts can be reported on this kind.

Completely different schedules, akin to Schedule D (capital features and losses) and Schedule Ok-1, are additionally hooked up to Kind 1041 to report particular forms of earnings or the beneficiary’s share of earnings.

How does Kind 1041 differ from Kind 1040?

Kind 1040 is used to report the earnings of a person taxpayer, whereas Kind 1041 is used for the decedent’s property or a belief. For instance:

- Kind 1040 covers the earnings earned by a person earlier than their date of loss of life.

- Kind 1041 handles earnings earned by the property or belief after the person’s loss of life.

For instance, if somebody dies earlier than receiving their ultimate paycheck, the cash from that paycheck will likely be transferred to their property. This earnings must be reported on Kind 1041. However somebody should additionally file a ultimate return (Kind 1040) for the deceased — often a partner, one other shut relative, or an legal professional. This may report all their earnings earned within the ultimate tax yr whereas they had been alive.

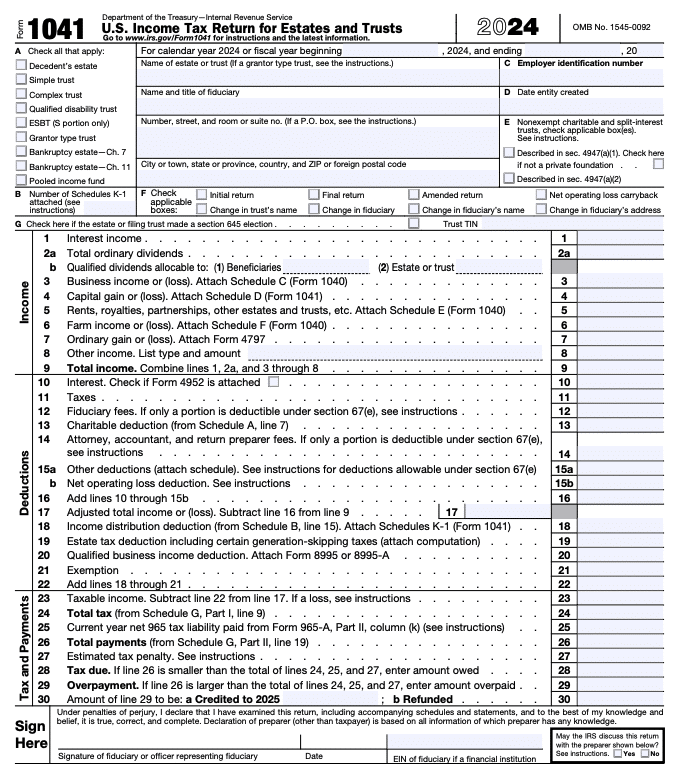

Kind 1041 instance

Right here’s what the primary web page of IRS Kind 1041 appears like:

Ensure that to collect all of the monetary paperwork essential to help the tax deductions you wish to declare on Kind 1041. For assist with this, take a look at our Form 1041 tax preparation checklist.

Kind 1041 directions: Who must file Kind 1041?

The fiduciary (executor, administrator, or trustee) managing the property or belief is answerable for submitting Kind 1041 to report any earnings tax legal responsibility of the property or belief.

You need to file Kind 1041 if the property or belief meets any of the next standards.

Decedent’s property

The fiduciary (or one of many joint fiduciaries) should file Kind 1041 for a home property that has:

- Gross earnings for the tax yr of $600 or extra, or

- A beneficiary who’s a nonresident alien.

- If you happen to held a certified funding in a certified alternative fund (QOF) at any time in the course of the yr, you will need to file your return with Form 8997 hooked up.

If the property generates no taxable earnings and has no nonresident alien beneficiaries, there’s no must file Kind 1041.

An property is a home property if it isn’t a international property. A international property earns earnings from sources outdoors the USA. This earnings just isn’t related to any commerce or enterprise within the U.S. and isn’t a part of gross earnings. In case you are the fiduciary of a international property, file Kind 1040-NR, U.S. Nonresident Alien Revenue Tax Return, as a substitute of Kind 1041.

Belief

The fiduciary (or one of many joint fiduciaries) should file Kind 1041 for a home belief taxable under section 641 of the Inside Income Code that has:

- Any taxable earnings for the tax yr,

- Gross earnings of $600 or extra (no matter taxable earnings), or

- A beneficiary who’s a nonresident alien.

- If you happen to held a certified funding in a certified alternative fund (QOF) at any time in the course of the yr, you will need to file your return with Kind 8997 hooked up.

A belief is a home belief if it meets each of the next assessments:

- Courtroom check: A U.S. courtroom can train major supervision over the belief administration.

- Management check: A number of U.S. individuals have the authority to manage all substantial selections of the belief.

A belief that isn’t a home belief will get handled as a international belief. In case you are the trustee of a international belief, you will need to file Kind 1040-NR as a substitute of Kind 1041. Additionally, a international belief with a U.S. proprietor typically should file Form 3520-A, Annual Data Return of International Belief With a U.S. Proprietor.

Exceptions

If the belief (or a portion of the belief) is a grantor sort belief, it should comply with particular reporting necessities outlined by the IRS in Instructions for Form 1041 and Schedules A, B, G, J, and K-1, web page 13. Grantor trusts permit the grantor (the individual or individuals who created the belief) to have sure powers and possession advantages. Grantor trusts are typically ignored for earnings tax functions, and the IRS considers the earnings, deductions, and many others., as belonging to the grantor.

Observe: Two or extra trusts are handled as one belief if the principle purpose for the trusts is to keep away from paying taxes AND they’ve the identical grantors and beneficiaries. This rule solely applies to the portion of the belief that comes from contributions (belongings added to the belief) after March 1, 1984. In different phrases, any cash or property added to the belief after that date will likely be topic to this “combining” rule if the factors are met.

Revenue to report on Kind 1041

Revenue for Kind 1041 consists of cash earned by the property or belief from sources akin to:

It’s important to separate earnings earned earlier than and after the date of loss of life, as solely the latter is reported on Kind 1041. The previous will get reported on Kind 1040.

Widespread deductions for estates and trusts

Here’s a quick record of frequent tax deductions and exemptions that may decrease the property’s taxable earnings:

- $600 exemption

- Executor charges (deductible if the property pays the executor for his or her companies)

- Skilled charges for lawyer and accountant prices

- Administrative bills, akin to courtroom submitting charges

- Required distributions to beneficiaries

- Charitable contributions made by the property or belief

When claiming deductions or tax credit, be aware that you could be additionally must file Schedule I, which is used to determine different minimal tax for estates and trusts.

The way to calculate the earnings distribution deduction for Kind 1041

The earnings distribution deduction permits an property or belief to cut back its taxable earnings by the quantity of earnings it distributes to its beneficiaries in the course of the tax yr. This deduction ensures that earnings is taxed solely as soon as — on the beneficiary’s stage — quite than each the belief and beneficiary being taxed on the identical earnings.

To calculate this deduction, use the distributable internet earnings (DNI) as the utmost restrict. DNI represents the property or belief’s complete earnings minus sure allowable deductions like charitable deductions and bills for administering the property. Distributions to beneficiaries can’t exceed the DNI quantity. To keep away from errors on Kind 1041 and Schedule Ok-1, be sure to correctly assign earnings and doc the way it was distributed.

Kind 1041 FAQs

Reporting earnings from estates and trusts: The way to file Kind 1041 with TaxAct

Submitting Kind 1041 doesn’t must be difficult! TaxAct’s intuitive tax software program guides you thru the method step-by-step, making certain you meet all of the filing requirements whereas serving to you maximize any tax deductions or credit accessible to the property or belief.

Head over to TaxAct Estates and Trusts to get began. If you happen to need assistance in the course of the tax submitting course of, we even have detailed directions for:

Want extra time to file Kind 1041? Don’t overlook that TaxAct may show you how to file an extension for Kind 1041 by submitting Kind 7004 to the IRS. Coping with property and belief taxes is taxing sufficient — this ensures you’ll be able to take the mandatory time to arrange whereas avoiding penalties for late submitting.

The underside line

Submitting taxes for an property or belief will not be your concept of enjoyable. However with TaxAct’s assist, it doesn’t must really feel not possible. By understanding Kind 1041 and staying organized, you’ll conquer your earnings tax return like a professional this yr.