The quantity of taxes you pay has a big influence in your take-home earnings, however there are a number of methods you should utilize to cut back your taxable earnings and lower your expenses.

The mortgage curiosity deduction is one among a number of tax deductions you might qualify for. If you happen to make mortgage funds on your property, you could possibly declare the curiosity paid as a write-off to cut back your tax invoice.

If you happen to’re a house owner and also you’re not profiting from the householders’ curiosity deduction, you might be lacking out on essential tax financial savings. Be taught extra in regards to the mortgage curiosity deduction and discover out if you happen to qualify.

How does the mortgage curiosity deduction work?

The mortgage curiosity deduction is a tax deduction you should utilize to jot down off the mortgage curiosity you pay all year long.

Every time you make your own home cost, a portion of that cost goes to curiosity and the remainder goes towards the principal quantity. On the finish of the 12 months, you may account for the entire mortgage curiosity you’ve paid and deduct some or all of it in your tax return.

Nevertheless it’s not so simple as a fast calculation; there are additionally sure circumstances that should be met to assert this deduction, which we’ll cowl in additional element beneath.

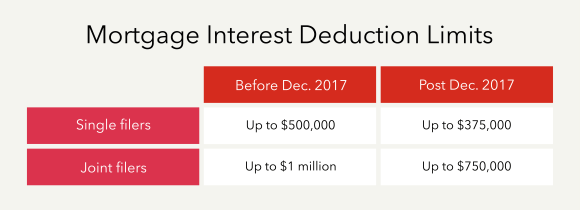

Dwelling mortgage deduction restrict

If you happen to just lately purchased a house, you’re most likely questioning how a lot you may deduct. Luckily, most householders are in a position to deduct all the mortgage curiosity they pay annually.

The mortgage curiosity deduction restrict is $750,000, or $375,000 if you happen to’re married submitting individually. This implies you may deduct mortgage curiosity on the primary $750,000 or $375,000 of debt, respectively. As such, many householders are in a position to deduct 100% of their mortgage curiosity.

If you happen to’re deducting mortgage curiosity for a mortgage that started earlier than December 16, 2017, you may deduct the curiosity paid on the primary $1 million ($500,000 if married submitting individually) of debt.

What properties qualify for this deduction?

There are a number of necessities a property has to fulfill to qualify for the mortgage curiosity deduction. Typically talking, you may deduct mortgage curiosity in your major house or your second house. The mortgage should have been obtained in “buying, developing, or considerably enhancing” the residence and should be secured by the house.

You may solely have one major residence, or essential house, without delay. That is the house the place you reside many of the 12 months. Your major residence can embody a:

- Home

- Condominium

- Cooperative

- Cell house

- Home trailer

- Boat

If you happen to personal a second house, you might also be capable to deduct mortgage curiosity funds. If you happen to don’t hire your second house out, you may deal with it as a certified house even if you happen to don’t stay there at any level throughout the 12 months.

For a second house or trip house that you just’re renting out, you must use it for a part of the 12 months to qualify for the householders’ curiosity deduction. You could use your second house for 14 days or 10% of the variety of days it was rented out, whichever is longer.

The mortgage curiosity could be prorated between private use (itemized deductions) and rental days (rental bills). If the house qualifies as a rental property, the mortgage curiosity can be deducted in opposition to rental earnings on Schedule E.

When you have a number of properties, you may solely designate one essential house and one second house. Nonetheless, there are some circumstances the place you may designate a distinct house as your second house throughout the 12 months.

Mortgage curiosity deduction instance

Let’s check out a mortgage curiosity deduction instance so you may see how this deduction would possibly apply to you. If you happen to pay $850 per thirty days in mortgage curiosity, that’s $10,200 per 12 months.

If you happen to’re married submitting collectively, the usual deduction for tax 12 months 2024 is $29,200. Until you’ve gotten practically $30,000 in deductible bills, you wouldn’t itemize and make the most of the mortgage curiosity deduction.

Mortgage curiosity deduction for second properties

Is mortgage curiosity tax deductible on a second house? The brief reply is sure, however there are particular necessities your second house has to fulfill to be eligible.

Let’s say you latterly bought a trip house, and also you wish to deduct your mortgage curiosity. You are able to do that so long as that trip house is designated as your second house and meets the certified house necessities.

If you happen to don’t hire out your second house, you don’t must do something to deal with it as a certified house. You additionally don’t have to fret about spending a sure variety of days on the property to qualify for the deduction.

If you happen to hire out your second house, you must use it for greater than 14 days or 10% of the variety of days it’s rented out, whichever is longer. If you happen to don’t meet this requirement, your second house can be thought of a rental property, and the mortgage curiosity can be deductible in opposition to the rental earnings.

Individuals who have multiple second house can select which house they wish to designate as a certified house. You may solely deal with one further house as a certified second house, and it has to fulfill the usual certified house necessities.

If the home is in each of your names, you’re each usually entitled to assert the mortgage curiosity deduction in your taxes. You don’t have to assert this deduction.

If you happen to’re each making mortgage funds, you may every deduct the portion of the mortgage curiosity you paid.

When just one individual makes mortgage funds however the 1098 has two names on it, solely the one that made the funds is entitled to assert the curiosity deduction. This individual can declare the complete quantity on Type 1098.

For spouses submitting separate returns, you may every designate separate properties because the certified house. Each spouses may consent to the first and secondary properties being designated by one partner.

The impact of refinancing on the mortgage curiosity deduction

Typically talking, you’re nonetheless eligible to assert the mortgage curiosity deduction if you happen to refinanced. You’ll pay mortgage curiosity in your refinanced mortgage, which implies you’re eligible for the deduction.

If you happen to paid mortgage factors once you refinanced your mortgage, you could possibly deduct them. Every level is the same as 1% of the mortgage quantity. Lenders use a number of names to confer with factors, together with:

- Lender origination charge

- Most mortgage cost

- Low cost factors

- Mortgage low cost

If you deduct mortgage factors in your taxes, you must deduct them over the lifetime of the mortgage. If you happen to pay factors on a 15-year mortgage, you may deduct a portion of the factors you paid for every of these 15 years.

Settlement charges are additionally a typical a part of refinancing a mortgage, however you don’t get a break on these. You sometimes can’t deduct settlement charges in a mortgage refinance, which incorporates issues like:

- Appraisal charges

- Lawyer charges

- Inspection charges

- Authorized and recording charges

deduct your mortgage curiosity in your taxes

Deducting mortgage curiosity in your taxes begins with submitting an itemized return, which implies you’ll want Type 1040 (Schedule A) along with the usual 1040 type.

If taxpayers have complete itemized deductions larger than their normal deduction, they might select to obtain the larger tax profit by itemizing.

Begin by finishing Schedule A. There are a handful of strains you wish to give attention to once you’re deducting mortgage curiosity and factors:

- Line 8a: Dwelling mortgage curiosity and factors reported to you on Type 1098

- Line 8b: Mortgage curiosity not reported to you on Type 1098

- Line 8c: Factors not reported to you on Type 1098

- Line 8d: Reserved for future use

- Line 8e: Add strains 8a by means of 8c

Line 8e can be your complete deduction for mortgage curiosity and factors. When you full Schedule A and add up all of your deductions, you may write that complete on line 12 of Type 1040.

Understand that the IRS expects you to take care of information for all the itemized bills you declare in your tax return. It’s vital to hold onto receipts, payments, and canceled checks for any bills you’re deducting.