Key Findings

- A capital allowanceA capital allowance is the quantity of capital funding prices, or cash directed in direction of an organization’s long-term progress, a enterprise can deduct every year from its income by way of depreciation. These are additionally generally known as depreciation allowances.

is the quantity of capital funding prices a enterprise can deduct from its income by way of the taxA tax is a compulsory cost or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of common authorities companies, items, and actions.

code by way of depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, akin to equipment or a manufacturing unit, to find out the multiyear interval over which the price of that asset might be deducted from taxable revenue. As an alternative of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, decreasing their worth and discouraging funding.

. - Ideally, international locations ought to present increased capital allowances, as they’ll increase enterprise funding which, in flip, spurs financial progress.

- The typical of OECD international locations’ capital allowances step by step decreased between 2000 and 2017, however then elevated between 2018 and 2022. In 2023, capital allowances declined once more.

- Many short-term measures of accelerated depreciation launched in response to the pandemic-induced financial disaster expired in 2023, with extra set to run out within the coming years. If these adjustments aren’t renewed and made everlasting, companies may take into account suspending or decreasing funding.

- Even comparatively low charges of inflationInflation is when the overall value of products and companies will increase throughout the economic system, decreasing the buying energy of a forex and the worth of sure property. The identical paycheck covers much less items, companies, and payments. It’s generally known as a “hidden tax,” because it leaves taxpayers much less well-off because of increased prices and “bracket creep,” whereas rising the federal government’s spending energy.

can considerably scale back the values of deductions for long-term investments. A rise in inflation from 2 p.c to six.9 p.c, the typical inflation fee within the OECD in 2023, reduces the funding prices companies can get better by as much as 11.4 proportion factors. - Excessive inflation and rates of interest create strain on enterprise funding, and Mexico and Israel are presently the one OECD international locations that modify capital allowances for inflation.

- A number of smaller OECD international locations not solely enable increased capital allowances but additionally levy decrease company revenue taxA company revenue tax (CIT) is levied by federal and state governments on enterprise income. Many firms aren’t topic to the CIT as a result of they’re taxed as pass-through companies, with revenue reportable underneath the person revenue tax.

charges, making them extra enticing for capital funding.

Introduction

The continued financial uncertainty from Russia’s warfare in Ukraine, post-pandemic financial restoration, provide chain disruptions, and rising rates of interest have highlighted the significance of funding. Policymakers all over the world are working to help important infrastructure, transition to an environmentally sustainable economic system, and kit their financial insurance policies towards progress.

In 2019, non-public sector funding in OECD international locations outpaced public funding by 5 to 1. In accordance with knowledge from the Worldwide Financial Fund (IMF), the typical OECD nation noticed almost $300 billion in non-public funding in comparison with $55 billion in public funding. Guaranteeing a steady setting for enterprise funding can be important within the coming years.[1]

Though generally neglected in discussions about company taxation, capital value restorationValue restoration is the power of companies to get better (deduct) the prices of their investments. It performs an vital function in defining a enterprise’ tax base and may influence funding choices. When companies can not absolutely deduct capital expenditures, they spend much less on capital, which reduces employee’s productiveness and wages.

performs an vital function in defining a enterprise’s company tax baseThe tax base is the entire quantity of revenue, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slender tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges.

and may influence these funding choices—with far-reaching penalties. When companies aren’t allowed to totally deduct capital expenditures in actual phrases, they make fewer capital investments, which additionally reduces employee productiveness and wages.[2] Thus, companies ought to be allowed to totally deduct their capital investments in actual phrases—both by way of full expensingFull expensing permits companies to right away deduct the total value of sure investments in new or improved know-how, tools, or buildings. It alleviates a bias within the tax code and incentivizes firms to speculate extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs.

or impartial value restoration.[3]

Capital value restoration varies significantly throughout OECD international locations, starting from one hundred pc in actual phrases in Estonia and Latvia to solely 41.7 p.c in Chile and 53 p.c in New Zealand (masking industrial buildings, equipment, and intangibles). After years through which many OECD international locations modified their capital allowance guidelines as a result of pandemic, most of the short-term measures of accelerated depreciation ended or began phasing out in 2023.

On common, companies within the OECD can get better 68.6 p.c of the price of capital investments in actual phrases. Investments in equipment get pleasure from the most effective remedy, with an OECD common of 85.3 p.c, adopted by intangibles (76.4 p.c) and industrial buildings (48 p.c). In 2000, companies had been in a position to get better on common 70.4 p.c of capital funding prices within the OECD, adopted by a gradual decline after which a rise starting in 2018.

Inflationary pressures and excessive rates of interest lower the worth of capital value allowances and thus improve the price of new investments. For consistency, this report assumes an inflation fee of two p.c, however such a low inflation fee is uncommon within the present economic system. Mexico and Israel are presently the one OECD international locations to regulate capital allowances for inflation.

Since 2000, statutory company revenue tax charges have declined considerably the world over and in OECD international locations.[4] Nonetheless, as the typical tax remedy of capital investments worsened for many of the final twenty years, the advantages of decrease statutory charges for funding and progress had been partially offset. This broadening of tax bases by way of decrease capital allowances is without doubt one of the the reason why company tax revenues had been rising or had been steady all over the world regardless of declining statutory charges.[5]

The Fundamentals of Depreciation Schedules and Capital Allowances

Earlier than exploring the information extra carefully, it’s price understanding a few of the terminology used on this space of company taxation:

- Governments set depreciation schedules to outline how companies can deduct their capital funding prices from their revenues over a number of years.

- The quantity of funding prices a enterprise can deduct in a yr is known as a capital allowance.

- Full expensing permits companies to deduct the total value of a capital funding within the yr of acquisition quite than following a multiyear depreciation schedule.

- Accelerated depreciation or bonus depreciationBonus depreciation permits companies to deduct a bigger portion of sure “short-lived” investments in new or improved know-how, tools, or buildings within the first yr. Permitting companies to jot down off extra investments partially alleviates a bias within the tax code and incentivizes firms to speculate extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs.

will increase capital allowances in earlier years and is commonly used to stimulate funding throughout financial downturns. - Capital value restoration charges replicate the web current worth of capital allowances a enterprise can deduct for a given capital funding over the total depreciation interval.

Companies decide their income by subtracting prices (akin to wages, uncooked supplies, and tools) from income. Nonetheless, in most jurisdictions, capital investments aren’t handled like different prices that may be subtracted from income within the yr that the cash is spent. This introduces a bias towards short-term initiatives, with little or no capital funding.

As an alternative, depreciation schedules specify the life span of an asset—usually derived from the financial lifetime of an asset—and decide the variety of years over which an asset have to be written off. By the top of the depreciation interval, the enterprise would have deducted the preliminary greenback value of the asset.[6] Nonetheless, most often, depreciation schedules don’t take into account the time worth of cash (a traditional return plus inflation).[7]

Depreciation schedules might be based mostly on completely different strategies, with straight-line depreciation and declining-balance depreciation the commonest. The strategies outline how annual capital allowances are calculated. Whereas the straight-line methodology depreciates an asset by an equal allowance every year, the declining-balance methodology bases the annual allowance on the remaining e-book worth of the asset. (See the Appendix for instance calculations.)

Such depreciation schedules outline how a lot of capital funding prices a enterprise can deduct in actual phrases. As an example, assume a machine prices $10,000 and is topic to a life span of 10 years. Underneath straight-line depreciation, a enterprise may deduct $1,000 yearly for 10 years. Nonetheless, as a result of time worth of cash, a deduction of $1,000 in later years shouldn’t be as precious in actual phrases as right this moment’s deduction. If inflation is 2 p.c and the required actual return on funding is 5.5 p.c, then on the finish of the 10-year interval, the worth of that final deduction can be simply $522 in right this moment’s phrases. In complete, the enterprise will solely be capable to deduct $7,379 as an alternative of the total $10,000, simply 73.8 p.c of the entire. This understates true enterprise prices and inflates taxable income, successfully taxing income that don’t exist.

This impact is exacerbated by longer depreciation schedules and better inflation or increased rates of interest. Decrease capital allowances, and thus the next value of capital, can result in a decline in enterprise funding, reductions within the productiveness of capital, and decrease wages.[8]

Capital allowances might be expressed as a proportion of the web current worth of funding prices that companies can write off over the lifetime of an asset—the so-called capital value restoration fee. A one hundred pc capital value restoration fee represents a enterprise’s capacity to deduct the total value of the funding (together with a traditional return plus inflation) over its life (e.g., by way of full expensing or impartial value restoration). A capital value restoration fee above one hundred pc represents the chance for companies to deduct greater than the total value of an funding. The decrease the capital value restoration fee, the extra a enterprise’s taxable revenueTaxable revenue is the quantity of revenue topic to tax, after deductions and exemptions. For each people and firms, taxable revenue differs from—and is lower than—gross revenue.

is inflated and the extra its tax invoice is overstated, making capital funding dearer.

Capital Allowances and Financial Development

Though generally neglected as a extra technical situation, capital allowances can have vital financial impacts. Relying on their construction, they’ll both increase or gradual funding which, in flip, impacts financial progress.

Decrease Capital Allowances Result in Slower Financial Development

Any value restoration system that doesn’t enable the total write-off of an funding—full expensing—within the yr the funding is made denies restoration of part of that funding, inflates the taxable revenue, and will increase the taxes paid by companies.[9] Decrease capital allowances improve the price of capital, which ends up in slower funding and a discount of the capital inventory, decreasing productiveness, employment, and wages.[10]

Prior analysis has discovered proof that funding is delicate to adjustments in the price of capital. In a literature assessment, economists Kevin Hassett and R. Glenn Hubbard discovered “a consensus has emerged [among economists] that funding demand is delicate to taxation.” In different phrases, because of both longer asset lives or the next company revenue tax fee, the demand for capital decreases and ranges of funding decline, decreasing the expansion within the capital inventory.[11] A 2023 examine finds that funding can also be delicate to inflation. In a state of affairs with a company tax fee of twenty-two p.c, a depreciation fee of 25 p.c, and an inflation fee of two p.c, a one-percentage-point improve in inflation reduces the optimum funding degree by 0.42 p.c.[12] A discount within the capital inventory results in decrease wages for employees and slower financial progress.[13]

In recent times, extra empirical outcomes on such funding results have emerged. A 2017 examine by economists Eric Zwick and James Mahon exhibits that bonus depreciation carried out in the US raised funding in eligible capital relative to ineligible capital by 10.4 p.c between 2001 and 2004 and by 16.9 p.c between 2008 and 2010. As well as, their findings confirmed that small companies are dramatically extra delicate to the coverage change than massive companies.[14]

A examine carried out by economists Giorgia Maffini, Jing Xing, and Michael P. Devereux estimates the impact of accelerated depreciation allowances the UK launched in 2004. Their outcomes present that “the funding fee of qualifying firms elevated 2.1-2.5 proportion factors relative to those who didn’t qualify.”[15] Economists Yongzheng Liu and Jie Mao discovered that China’s swap from a production-based VAT to a consumption-based VAT—which means there’s now an funding tax credit scoreA tax credit score is a provision that reduces a taxpayer’s remaining tax invoice, dollar-for-dollar. A tax credit score differs from deductions and exemptions, which scale back taxable revenue, quite than the taxpayer’s tax invoice straight.

—additionally had a optimistic impact on funding.[16]

Unequal Capital Allowances Create a Distortion amongst Completely different Investments within the Economic system

It’s also vital to notice that capital allowances can distort the relative prices of various investments and thus alter the combination of capital in an economic system. A authorities may lengthen depreciation schedules for equipment, which might gradual funding in equipment, harming the manufacturing trade. Likewise, if depreciation schedules are shortened, or if companies are allowed expensing of equipment, this improve in capital allowances could spur extra equipment funding relative to different funding within the nation.

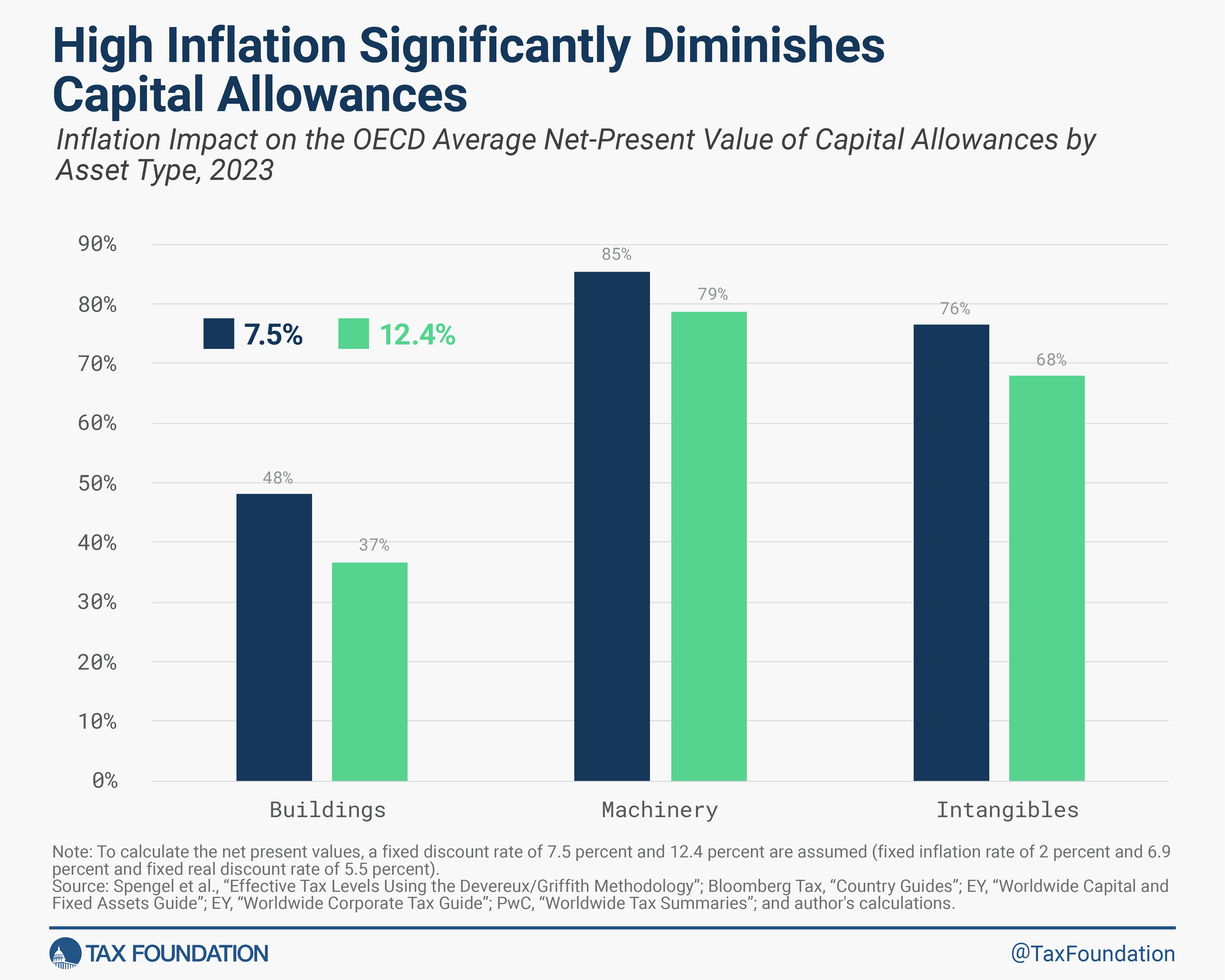

Wanting on the common capital value restoration fee in OECD international locations by asset sort, stark variations are evident. Companies within the OECD are in a position to get better on common 85.3 p.c of funding prices in equipment and 76.4 p.c in intangibles, however solely 48 p.c for buildings.

Moreover, in high-inflation situations like the present one—the place the OECD annual inflation was 6.9 p.c in 2023—the funding quantity companies are in a position to get better is considerably diminished.[17] If inflation is 6.9 p.c and the required actual return on funding is 5.5 p.c, then companies within the OECD will be capable to get better on common solely 36.5 p.c for buildings, 78.6 p.c for equipment, and 67.6 p.c for intangibles. Subsequently, a rise in inflation from 2 p.c to six.9 p.c reduces the quantity of funding that may be recovered by as much as 11.4 proportion factors. However even comparatively low charges of inflation can considerably scale back the values of deductions for long-term investments. Equally, excessive rates of interest scale back the worth of deductions over time by rising the required actual return on funding.

Tax adjustments in the US have given preferential tax remedy to sure property over others, which has led to adjustments within the composition of funding. In 2003, the US handed the Jobs and Development Tax Aid Reconciliation Act of 2003 (JGTRRA). A part of this legislation allowed for partial expensing of sure capital tools, rising capital allowances and decreasing the price of different capital investments by as a lot as 11.4 p.c.[18] Analysis on this alteration discovered that “funding elevated probably the most for tools with an extended restoration interval and that ‘bonus depreciation had a strong impact on the composition of funding.’”[19]

If a rustic cuts its company tax fee whereas limiting capital allowances, it will probably result in a shift within the economic system from extra capital-intensive industries to sectors that rely much less on capital funding. That is the case within the 2010s within the UK, which traded longer asset lives for a decrease company tax fee and noticed enterprise funding endure.[20] The differential remedy of capital-intensive industries over different sectors has seemingly contributed to the worsening of traits which have revealed important variations in regional financial output within the UK.[21]

Capital Allowances within the OECD

The remedy of capital allowances varies significantly throughout OECD international locations. The bottom-ranking nation, Chile, permits its companies to get better on common solely 41.7 p.c of capital funding prices, whereas the highest-ranking international locations—Estonia and Latvia—enable their companies to get better one hundred pc. This wide selection is basically because of international locations’ vastly completely different company tax constructions, depreciation schemes, and incentives designed to prioritize sure asset varieties over others.

Funding in industrial buildings has comparatively poor tax remedy within the OECD, with a median allowance of solely 48 p.c. Estonia and Latvia have the most effective remedy of commercial buildings at one hundred pc, because of their cash-flow tax methods. The international locations with the bottom capital value restoration charges for industrial buildings are Costa Rica, Hungary, and Japan, with 27.9 p.c every.

Equipment typically has the most effective tax remedy, with an OECD common allowance of 85.3 p.c. Canada and the UK are presently above common, at one hundred pc, because of full expensing of investments in equipment. These insurance policies had been made everlasting in the UK however phased out in Canada. Estonia and Latvia even have full value restoration of investments in equipment, once more because of their cash-flow tax methods. Of the international locations with out full expensing, the US (97.5 p.c) and the Czech Republic (97.2 p.c) presently provide probably the most beneficiant capital allowances because of short-term insurance policies of accelerated depreciation. The international locations with the worst tax remedy of investments in equipment are Chile (63.3 p.c) and New Zealand (73.2 p.c).

The typical capital allowance for intangibles is 76.4 p.c in OECD international locations. Estonia and Latvia lead at one hundred pc. Of the international locations with deductions for intangible property, Canada has the worst tax remedy of investments in intangibles, at 51.9 p.c, adopted by Australia, New Zealand, and Portugal (all 54.8 p.c) and the US (63.3 p.c). Chile doesn’t present allowances for intangible property.

The next map exhibits that the extent to which companies can deduct their capital funding prices varies significantly throughout Europe.

Non permanent Measures of Accelerated Depreciation

To spur capital funding throughout financial downturns, policymakers usually briefly improve capital allowances. A number of OECD international locations have completed so in response to the pandemic-induced financial disaster and post-pandemic gradual financial progress.

- Australia carried out two short-term depreciation measures within the first half of 2020 that apply to all companies with revenues under AUD 500 million (USD 333 million), particularly an on the spot asset write-off (full expensing) for depreciating property that value lower than AUD 150,000 (up from AUD 30,000) and an accelerated depreciation deduction for all depreciable property that aren’t eligible for the immediate write-off. On the finish of 2020, Australia carried out short-term full expensing for many property (excluding buildings) for companies with revenues under AUD 5 billion (USD 3.3 billion). These short-term measures will expire on 30 June 2023.[22]

- Austria accelerated depreciation for buildings within the first two years and permits companies to depreciate equipment at the next fee utilizing the declining-balance methodology. No finish date for these accelerated depreciation strategies has been set thus far. Moreover, an on the spot asset write-off (full expensing) is on the market for depreciating property that value lower than EUR 1,000 (USD 1,075).

- Chile allowed full expensing of mounted property—akin to buildings and equipment—and one hundred pc amortization of intangibles till the top of 2022, making it the third OECD nation after Estonia and Latvia that successfully offered full expensing for industrial buildings, equipment, and intangibles. With the phaseout of this coverage in 2023, the worth of Chile’s capital allowances returned from the best to the bottom within the OECD.

- The Czech Republic utilized extraordinary depreciation of equipment for the years 2020 to 2023, permitting companies to deduct 60 p.c of funding prices within the first yr and 40 p.c within the second yr.[23] The availability expires in 2024.

- Denmark made a “tremendous deduction” obtainable on prices regarding analysis and improvement. On account of COVID-19, the deduction fee is elevated in 2021, which means that prices linked to analysis and improvement might be deducted at a fee of 130 p.c in 2021, 105 p.c in 2022, 108 p.c in 2023-2025, and 110 p.c from 2026 onward. The “super-deductionA brilliant-deduction is a tax deduction that allows companies to deduct greater than one hundred pc of their eligible bills from their taxable revenue. As such, the super-deduction is successfully a subsidy for sure prices. This coverage generally applies to capital prices or analysis and improvement (R&D) spending.

” is conditioned on the prices being linked to the taxpayer’s enterprise. The deduction might be made both without delay within the revenue yr through which the prices are incurred, or over the course of 5 years, together with the revenue yr through which the prices are incurred. In 2023, Denmark decreased the straight-line fee of buildings depreciation from 4 p.c to three p.c.[24] - Finland doubled its declining-balance depreciation fee for equipment from 25 p.c to 50 p.c for the years 2020 to 2023. Not too long ago, the coverage was prolonged till the yr 2025.[25]

- Germany utilized accelerated depreciation schedules for equipment from 2020 to 2022. This provision expired in 2023 and was renewed for the yr 2024. The renewal was paired with accelerated depreciation for dwellings till 2029 and a everlasting improve within the on the spot asset write-offs for depreciating property that value lower than EUR 1,000 (USD 1,075).

- New Zealand briefly reintroduced depreciation for business and industrial buildings with an estimated helpful life of fifty years or extra from 2020 to 2023 and briefly elevated the edge for low-value property that qualify for rapid write-off. Constructing depreciation is about to be abolished once more in 2024.

- Norway has allowed for a right away deduction towards the particular tax base of latest investments in mounted property utilized in extractive actions topic to a particular oil tax since 2022.

- The United Kingdom completely reintroduced depreciation for industrial buildings at 2 p.c in 2019 and expanded it to three p.c in 2020. As well as, the UK considerably elevated capital allowances, permitting companies to deduct 130 p.c of the funding prices in plant and tools and 50 p.c for different investments, together with integral options to buildings between April 1, 2021, and March 31, 2023. The super-deduction expired on March 31, 2023, and was changed completely by full expensing, the coverage additionally mirrored on this report.[26]

Whereas the short-term nature of most of those expensing and accelerated depreciation provisions reduces their tax income influence in the long term, it additionally limits their long-run financial advantages. Non permanent provisions could encourage companies to shift future investments ahead to benefit from the bigger deductions however wouldn’t elevate the extent of funding completely. Thus, everlasting full expensing throughout all asset varieties—quite than focused short-term measures—would yield the best financial advantages.[27]

Capital Allowances in Chosen OECD International locations

Capital value restoration varies considerably throughout OECD international locations, as proven in Desk 1 above. The next examples spotlight a few of the variations and up to date developments.

Estonia and Latvia: Money-Movement Tax

Estonia and Latvia have each changed their conventional company revenue tax methods with a cash-flow tax mannequin, which permits for a capital value restoration fee of one hundred pc. Relatively than requiring firms to calculate their taxable revenue utilizing complicated guidelines and depreciation schedules on an annual foundation, the Estonian and Latvian company revenue tax of 20 p.c is levied solely when a enterprise distributes income to shareholders.

This not solely simplifies the calculation of taxable revenue, however it additionally permits for remedy of capital funding that’s equal to full expensing. Since distributed income are the tax base, there isn’t a want for depreciation schedules. As an alternative, capital prices scale back income within the yr of funding. This remedy of capital funding encourages companies in Estonia and Latvia to make use of their income to reinvest of their companies quite than distribute them to shareholders, resulting in new capital formation and elevated financial progress.

Canada and the US: Non permanent Expensing for Tools and Equipment

Presently, the US tax code permits companies to get better 66.7 p.c of capital funding prices on common, barely under the OECD common of 68.6 p.c.

The U.S. capital allowance for intangibles is 63.3 p.c, decrease than the OECD common of 76.4 p.c. Value restoration of nonresidential constructions can also be low within the U.S., at an allowance of solely 35 p.c over their quite lengthy 39-year asset lives, whereas the OECD common is 48 p.c.

For equipment, the U.S. presently has a 97.5 p.c capital value restoration fee because of short-term bonus depreciation offered by the Tax Lower and Jobs Act (TCJA) of 2017. Since 2023, the U.S. tax code solely offers 80 p.c bonus depreciation, set to say no by 20 proportion factors every subsequent yr till full phaseout. The OECD has a median of 85.3 p.c for capital allowances for equipment.

Notably, the OECD highlighted the U.S. provision in its 2018 Financial Survey of the US, mentioning that the coverage “will seemingly give a considerable increase to funding exercise.”[28] And it did. A 2022 examine discovered that TCJA elevated U.S. firms’ capital expenditures by roughly 0.2 p.c to 0.4 p.c of complete property when the imply capital expenditure of U.S. companies stands at 0.9 p.c.[29]

As a response to full expensing for equipment within the U.S., Canada adopted short-term full expensing for tools and equipment used within the manufacturing and processing of products, and for clear vitality investments.[30] These property could also be absolutely written off within the yr the tools or equipment is put into use, as an alternative of being depreciated over a number of years.

Canada additionally adopted accelerated depreciation schedules for non-residential buildings and intangible property.[31] Companies that spend money on buildings utilized in manufacturing and processing will be capable to write off 15 p.c of the associated fee within the first yr (up from 10 p.c), and first-year write-offs for investments in different nonresidential buildings have been elevated from 4 p.c to six p.c. For intangible property like patents, the declining steadiness fee has elevated from 5 to 7 p.c.

The TCJA offered one hundred pc bonus depreciation solely by way of 2022, declining by 20 proportion factors every year over the 2023 to 2026 interval; Canada’s enhanced deductions can be in place till 2023, with a gradual phaseout interval between 2024 and 2027. Though these reforms will briefly increase funding exercise, long-term results can be considerably increased if the adjustments had been made everlasting.[32]

United Kingdom Full Expensing

From April 2021 by way of the top of March 2023, UK companies may deduct 130 p.c of the prices of plant and tools (labeled “equipment” on this report). This coverage was meant to help enterprise funding within the transition from the earlier 19 p.c company tax fee to the present 25 p.c fee, which has been in place since April 2023. That’s a 130 p.c improve, matching the super-deduction.

The 2023 Spring Price range substituted the super-deduction with full expensing, shifting the UK allowance for plant and tools from a 130 p.c deduction to a one hundred pc deduction. This locations the UK in 15th place in Desk 1, whereas tying for first place for equipment. The short-term coverage leads to a whiplash impact for capital allowances, efficient tax charges, and general enterprise funding incentives. The 2023 Spring Price range additionally prolonged a 50 p.c first-year allowance to sure “integral options” and “long-life objects” that don’t qualify for full expensing. Additional, the Annual Funding Allowance (AIA)—which offers one hundred pc first-year aid for plant and equipment investments as much as GBP 1 million for all companies, together with unincorporated companies and most partnerships—was made a everlasting characteristic of the tax code.[33]

The 2023 Autumn Assertion made full expensing (and the 50 p.c first-year allowance) a everlasting characteristic of the tax code, averting an expiration of the coverage in 2026. Absent everlasting full expensing, the UK would have returned to an 18 p.c declining steadiness allowance for plant and tools, shifting from a one hundred pc deduction to a 75.8 p.c deduction (in web current worth phrases), and inserting the UK in 30th place general in Desk 1. Mannequin simulations by the Tax Basis and the Centre for Coverage Research estimate everlasting full expensing would elevate GDP by 0.9 p.c, funding by 1.5 p.c, and wages by 0.8 p.c, relative to a return to the pre-2021 legislation.[34]

Capital Value Restoration within the OECD since 2000

The straightforward common of OECD international locations’ capital value restoration charges decreased between 2000 and 2017, adopted by a slight improve in 2018 and 2019,[35] after which a major soar in 2020 and 2021 as a response to the COVID-19 pandemic. Whereas OECD international locations allowed their companies to deduct on common roughly 70.4 p.c of their capital investments in 2000, this quantity decreased to 66.7 p.c in 2014, reached its peak at 70.8 p.c in 2022, and declined to 68.6 p.c in 2023.

Weighted by GDP, the typical OECD capital value restoration fee declined barely from 2000 (65.4 p.c) to 2013 (63.8 p.c). After 2017, the development began rising rapidly. Full expensing for equipment in Canada and the US, the UK’s reintroduction of capital allowances for buildings and the super-deduction (now full expensing), and newly launched accelerated depreciation throughout asset varieties in a number of OECD international locations as a result of COVID-19 pandemic all contributed to elevating the weighted common within the final six years. In 2022, it peaked at 69 p.c, quickly declining to 67.1 p.c in 2023.

As Determine 4 exhibits, the OECD common capital value restoration fee weighted by every nation’s GDP is persistently decrease than the easy OECD common. It’s because smaller economies are likely to have higher tax remedy of capital funding. That is additionally mirrored in our rating (see Desk 1): Estonia, Latvia, Lithuania, the Czech Republic and Iceland—all comparatively small economies—are among the many international locations with the most effective tax remedy of capital investments.

Company Revenue Tax Charges within the OECD

Extra consideration is usually paid to the company revenue tax fee, quite than the revenue tax base. Nonetheless, the company revenue tax base and the company revenue tax fee are each vital in figuring out companies’ efficient tax ranges. Like low capital allowances, a excessive company revenue tax fee reduces firms’ after-tax income, will increase the price of capital, and slows the expansion of the capital inventory. This results in decrease productiveness, decrease wages, and slower financial progress.[36]

Prior to now 23 years, international locations all through the OECD have repeatedly decreased their statutory company revenue tax charges, pushing the typical fee in OECD international locations to roughly 23.6 p.c in 2023.[37] The OECD common of company revenue tax charges weighted by every nation’s GDP has additionally decreased since 2000, with a major decline between 2017 and 2018 as a result of reduce within the U.S. company revenue tax fee from about 32 p.c to 26 p.c.

Just like capital allowances, the OECD common of company revenue tax charges weighted by every nation’s GDP is persistently increased than the easy OECD common. This means that some smaller international locations are likely to not solely have increased capital allowances but additionally decrease company revenue tax charges, making them extra aggressive from a tax perspective than some bigger economies.

Conclusion

Though it has been vital to scale back the distortionary results of company revenue taxes by decreasing statutory charges all over the world, doing so with out additionally contemplating capital allowances misses an vital level of sound tax coverage. Low capital allowances scale back incentives to speculate, resulting in decrease wages and slower financial progress.

Moreover pursuing insurance policies of full expensing for capital investments, it is usually vital to make capital allowance provisions everlasting. Permanency implies certainty, which is an important issue for long-term funding choices. As an example, the short-term Canadian and U.S. expensing and accelerated depreciation provisions are more likely to spur financial progress within the quick time period. Their long-term results, nonetheless, can be a lot increased if the adjustments had been made everlasting, akin to in the UK.

Inflation and excessive rates of interest additionally create a problem for enterprise funding that’s exacerbated by lengthy depreciation schedules.

To get better from the pandemic and put the worldwide economic system on a trajectory for progress, policymakers have to goal for extra beneficiant and everlasting capital allowances. This may spur actual funding and may contribute to extra environmentally pleasant manufacturing throughout the globe.

Appendix

Calculating Capital Allowances: Straight-Line Technique

Appendix Desk 1 illustrates the calculation of a capital allowance utilizing the straight-line methodology. Suppose a enterprise made a capital funding of $100 and assume an actual low cost fee plus inflation that equals 7.5 p.c.

On this instance, the federal government permits funding in equipment to be deducted on a straight-line methodology of 12.5 p.c for eight years. This implies the enterprise can deduct 12.5 p.c of the preliminary value of an funding every year for eight years.

Yearly, the enterprise can deduct 12.5 p.c ($12.50) of the preliminary funding from taxable revenue. Within the first yr, the nominal worth equals the current worth of the write-off. Nonetheless, over time, the current worth of every yr’s write-off declines as a result of time worth of cash.

Though the nominal worth of your complete write-off is $100, the current worth is barely $78.71. Because of this, the corporate can solely get better 78.71 p.c of the current worth of the price of the machine by the top of the interval.

Now, suppose an inflation fee of 6.9 p.c. This may translate into an actual low cost fee plus inflation of 12.4 p.c. With the next inflation fee, though the nominal worth of your complete write-off is $100, the current worth is now solely $68.65. Because of this, the corporate can solely get better 68.65 p.c of the current worth of the price of the machine by the top of the interval.

Calculating Capital Allowances: Declining-Steadiness Technique

Appendix Desk 2 illustrates the calculation of a capital allowance utilizing the declining-balance methodology. Suppose a enterprise made a capital funding of $100 and assume an actual low cost fee plus inflation that equals 7.5 p.c.

Additionally, suppose the federal government permits funding in equipment to be deducted on a declining steadiness methodology of 20 p.c for eight years. This implies the enterprise can deduct 20 p.c of the remaining value of an funding every year and the residual quantity within the eighth yr.

Within the preliminary yr, the enterprise can deduct 20 p.c ($20) of the preliminary funding from taxable revenue. That $20 is subtracted from the preliminary worth of the machine. The following yr, the machine has a remaining worth of solely $80 (the preliminary $100 minus the 20 p.c deduction within the preliminary yr) and, as soon as once more, 20 p.c, or $16, is deducted from taxable revenue and subtracted from the worth of the machine. Within the subsequent yr, one other 20 p.c is deducted from the remaining $64 worth of the machine, or $12.80. This methodology continues till the ultimate yr, when the remaining $20.97 of the funding is deducted.

Over time, the web current worth of every yr’s write-off declines as a result of time worth of cash (actual low cost fee plus inflation). Though the nominal worth of your complete write-off is $100, the current worth is barely $80.94. Because of this, the corporate can solely get better 80.94 p.c of the current worth of the price of the machine by the top of the interval.

Now, suppose an inflation fee of 6.9 p.c. This may translate into an actual low cost fee plus inflation of 12.4 p.c. With the next inflation fee, though the nominal worth of your complete write-off is $100, the current worth is now solely $72.22. Because of this, the corporate can solely get better 72.22 p.c of the current worth of the price of the machine by the top of the interval.

International locations with Distinctive Depreciation Schedules

Whereas most OECD international locations observe both the straight-line or declining-balance depreciation strategies (or a mixture of each) to find out annual capital allowances, there are some notable exceptions. The Czech Republic and Slovakia have distinctive depreciation schedules, and Mexico and Israel enable companies to regulate their capital allowances for inflation.

Czech Republic and Slovakia: Particular Accelerated Depreciation Technique

Moreover the straight-line methodology, companies could elect to depreciate buildings (solely within the Czech Republic[38]) and equipment (in each international locations) utilizing a particular accelerated methodology. Underneath this methodology, depreciation for the primary yr is calculated by dividing the price of the asset by the variety of years reflecting the helpful lifetime of an asset. For subsequent years, accelerated depreciation is calculated by multiplying the residual tax worth of the asset by two after which dividing it by the remaining years of depreciation plus one yr.[39]

Regardless of this comparably complicated calculation of depreciation values, Slovakia ranks 11th (73.9 p.c) and the Czech Republic 5th (77.6 p.c) in our comparability of capital value restoration within the OECD, making them above common as locations for enterprise funding.[40]

Israel and Mexico: Inflation-Adjustment for Capital Allowances

Companies in Israel and Mexico are allowed to regulate their capital allowances for inflation—a novel characteristic amongst OECD international locations’ depreciation strategies.[41] This enables companies to get better a bigger share of their funding prices in actual phrases than they in any other case would, making it a partial type of impartial value restoration. Such inflation changes scale back the adverse influence of lengthy depreciation schedules on funding incentives and financial progress.

[1] IMF, “IMF Funding and Capital Inventory Dataset, 2021,” Could 2021, https://infrastructuregovern.imf.org/content/dam/PIMA/Knowledge-Hub/dataset/IMFInvestmentandCapitalStockDataset2021.xlsx.

[2] Stephen J. Entin, “The Tax Remedy of Capital Property and Its Impact on Development: Expensing, Depreciation, and the Idea of Value Restoration within the Tax System,” Tax Basis, Apr. 24, 2013, https://taxfoundation.org/tax-treatment-capital-assets-and-its-effect-growth-expensing-depreciation-and-concept-cost-recovery/.

[3] Stephen J. Entin, “The Impartial Value Restoration System: A Professional-Development Answer for Capital Value Restoration,” Tax Basis, Oct. 29, 2013, https://taxfoundation.org/article/neutral-cost-recovery-system-pro-growth-solution-capital-cost-recovery.

[4] OECD, “Desk II.1. Statutory company revenue tax fee,” up to date April 2023, https://stats.oecd.org/Index.aspx?DataSetCode=TABLE_II1.

[5] OECD, “Company Tax Statistics, Fifth Version” 2023, https://oecd.org/tax/beps/corporate-tax-statistics-database.htm.

[6] Stephen J. Entin, “The Tax Remedy of Capital Property and Its Impact on Development: Expensing, Depreciation, and the Idea of Value Restoration within the Tax System.”

[7] This may be regarded as the chance value of tying up the cash in a selected funding. See Stephen J. Entin, “The Impartial Value Restoration System: A Professional-Development Answer for Capital Value Restoration.”

[8] Stephen J. Entin, “The Tax Remedy of Capital Property and Its Impact on Development: Expensing, Depreciation, and the Idea of Value Restoration within the Tax System.”

[9] One other—though barely extra difficult—solution to obtain full value restoration is a impartial value restoration system. Underneath that system, write-offs are unfold over time, however the deferred quantities are elevated every year at a market rate of interest to protect a web current worth equal to expensing. See Stephen J. Entin, “The Impartial Value Restoration System: A Professional-Development Answer for Capital Value Restoration.”

[10] Stephen J. Entin, “The Tax Remedy of Capital Property and Its Impact on Development: Expensing, Depreciation, and the Idea of Value Restoration within the Tax System.”

[11] Kevin A. Hassett and R. Glenn Hubbard, “Tax Coverage and Enterprise Funding,” Handbook of Public Economics 3 (2002), https://sciencedirect.com/science/article/pii/S1573442002800246.

[12] Sebastian Beer, Mark Griffiths, and Alexander Klemm, “Tax Distortions from Inflation: What are they and How one can Take care of them?,” IMF Working Papers 23:18 (January 2023), https:// imf.org/en/Publications/WP/Issues/2023/01/27/Tax-Distortions-from-Inflation-What-are-They-How-to-Deal-with-Them-528666.

[13] Stephen J. Entin, “The Tax Remedy of Capital Property and Its Impact on Development: Expensing, Depreciation, and the Idea of Value Restoration within the Tax System.”

[14] Eric Zwick and James Mahon, “Tax Coverage and Heterogeneous Funding Habits,” American Financial Assessment 107:1 (January 2017): 217–248, https://aeaweb.org/articles?id=10.1257/aer.20140855.

[15] Giorgia Maffini, Jing Xing, and Michael P. Devereux, “The Influence of Funding Incentives: Proof from UK Company Tax Returns,” American Financial Journal: Financial Coverage 11:3 (August 2019): 361-89, https://aeaweb.org/articles?id=10.1257/pol.20170254.

[16] Yongzheng Liu and Jie Mao, “How Do Tax Incentives Have an effect on Funding and Productiveness? Agency-Stage Proof from China,” American Financial Journal: Financial Coverage 11:3 (August 2019): 261-91, https:// aeaweb.org/articles?id=10.1257/pol.20170478.

[17] OECD, “Shopper Value Indices (CPIs),” https://stats.oecd.org/Index.aspx?DataSetCode=PRICES_CPI.

[18] Kevin A. Hassett and Kathryn Newmark, “Taxation and Enterprise Habits: A Assessment of the Current Literature,” in John W. Diamond and George R. Zodrow, eds., Basic Tax Reform: Points, Decisions, and Implications (Cambridge, MA: MIT Press, 2008), 205.

[19] Id., at 206.

[20] Kyle Pomerleau, “Buying and selling Longer Asset Lives for Decrease Company Tax Charges in the UK,” Tax Basis, Jan. 29, 2014, https://taxfoundation.org/trading-longer-asset-lives-lower-corporate-tax-rates-united-kingdom/.

[21] Ben Gardiner, Ron Martin, Peter Sunley, and Peter Tyler, “Spatially Unbalanced Development within the British Economic system,” Journal of Financial Geography 13:6 (November 2013): 889-928.

[22] The info proven on this report displays capital allowances granted to all companies no matter measurement. As a result of income threshold, Australia’s accelerated depreciation and full expensing insurance policies aren’t mirrored within the knowledge.

[23] Grant Thornton, “Modification to the Revenue Tax Act – authorized entities,” Nov. 22, 2022, https://grantthornton.cz/en/news/amendment-to-the-income-tax-act-legal-entities/.

[24] EY, “Worldwide Company Tax Information 2023,” Sep. 5, 2023, https://www.ey.com/en_gl/tax-guides/worldwide-corporate-tax-guide.

[25] EY, “Worldwide Capital and Fastened Property Information 2023,” Jul. 12, 2023, https://www.ey.com/en_gl/tax-guides/worldwide-capital-and-fixed-assets-guide.

[26] Bloomberg Tax, “Hunt Says UK to Keep away from RecessionA recession is a major and sustained decline within the economic system. Sometimes, a recession lasts longer than six months, however restoration from a recession can take just a few years.

and Lower Inflation This Yr (1),” Mar. 15, 2023, https://news.bloombergtax.com/daily-tax-report-international/hunt-says-says-uk-to-avoid-recession-halve-inflation-this-year; Alex Mengden, “Full Expensing to Be Made Everlasting in the UK,” Tax Basis, Nov. 22, 2023, https://taxfoundation.org/weblog/uk-full-expensing-permanent/.

[27] For additional evaluation, see Kyle Pomerleau, “Financial and Budgetary Influence of Non permanent Expensing,” Tax Basis, Oct. 4, 2017, https://www.taxfoundation.org/economic-budgetary-impact-temporary-expensing/.

[28] OECD, “OECD Financial Surveys United States,” June 2018, https://read.oecd-ilibrary.org/economics/oecd-economic-surveys-united-states-2018_eco_surveys-usa-2018-en#page12.

[29] Steve Crawford and Garen Markarian, “The Impact of the Tax Cuts and Jobs Act of 2017 on Company Funding,” SSRN Digital Journal (October 6, 2020), http://dx.doi.org/10.2139/ssrn.4239855.

[30] Canada Income Company, “Accelerated funding incentive,” November 2023, https:// canada.ca/en/revenue-agency/services/tax/businesses/topics/sole-proprietorships-partnerships/report-business-income-expenses/claiming-capital-cost-allowance/accelerated-investment-incentive.html .

[31] Id.

[32] Kyle Pomerleau, “Financial and Budgetary Influence of Non permanent Expensing;” and William Gbohoui, “Do Non permanent Enterprise Tax Cuts Matter? A Basic Equilibrium Evaluation,” IMF, Feb. 15, 2019, https://www.imf.org/en/Publications/WP/Issues/2019/02/15/Do-Temporary-Business-Tax-Cuts-Matter-A-General-Equilibrium-Analysis-46524.

[33] HM Treasury, “Spring Price range 2023 – Full expensing,” up to date Jan. 30, 2024, https://gov.uk/government/publications/full-expensing/spring-budget-2023-full-expensing.

[34] Tom Clougherty, Kyle Pomerleau, and Daniel Bunn, “Non permanent Full Expensing Arrives within the UK,” Tax Basis, Mar. 17, 2023, https://taxfoundation.org/weblog/uk-budget-tax-reform-full-expensing/.

[35] The will increase in 2018 and 2019 are primarily as a result of introduction of short-term full expensing for equipment in Canada and the US, in addition to the reintroduction of capital allowances for industrial buildings in the UK.

[36] William McBride, “What Is the Proof on Taxes and Development?” Tax Basis, Dec. 18, 2012, https://www.taxfoundation.org/article/what-evidence-taxes-and-growth.

[37] OECD, “Desk II.1. Statutory company revenue tax fee.”

[38] In 2015, Slovakia switched from its distinctive accelerated depreciation methodology for buildings to the straight-line methodology. It stored its accelerated methodology for equipment.

[39] Instance: Within the first yr within the case of an asset with a helpful lifetime of six years, depreciation is 16.7 p.c (100/6). The next years, the residual worth is multiplied by two and divided by the remaining years of depreciation plus one yr; i.e., for the second yr: (100-16.7%) x 2 / (6-1+1) = 27.77%.

[40] For the years 2020 to 2023, the Czech Republic allowed the price of equipment to be written off by 60 p.c within the first yr and the rest within the second yr.

[41] EY, “Worldwide Capital and Fastened Property Information”, Jul. 12, 2023, https://ey.com/en_gl/tax-guides/worldwide-capital-and-fixed-assets-guide.

Share